Introduction

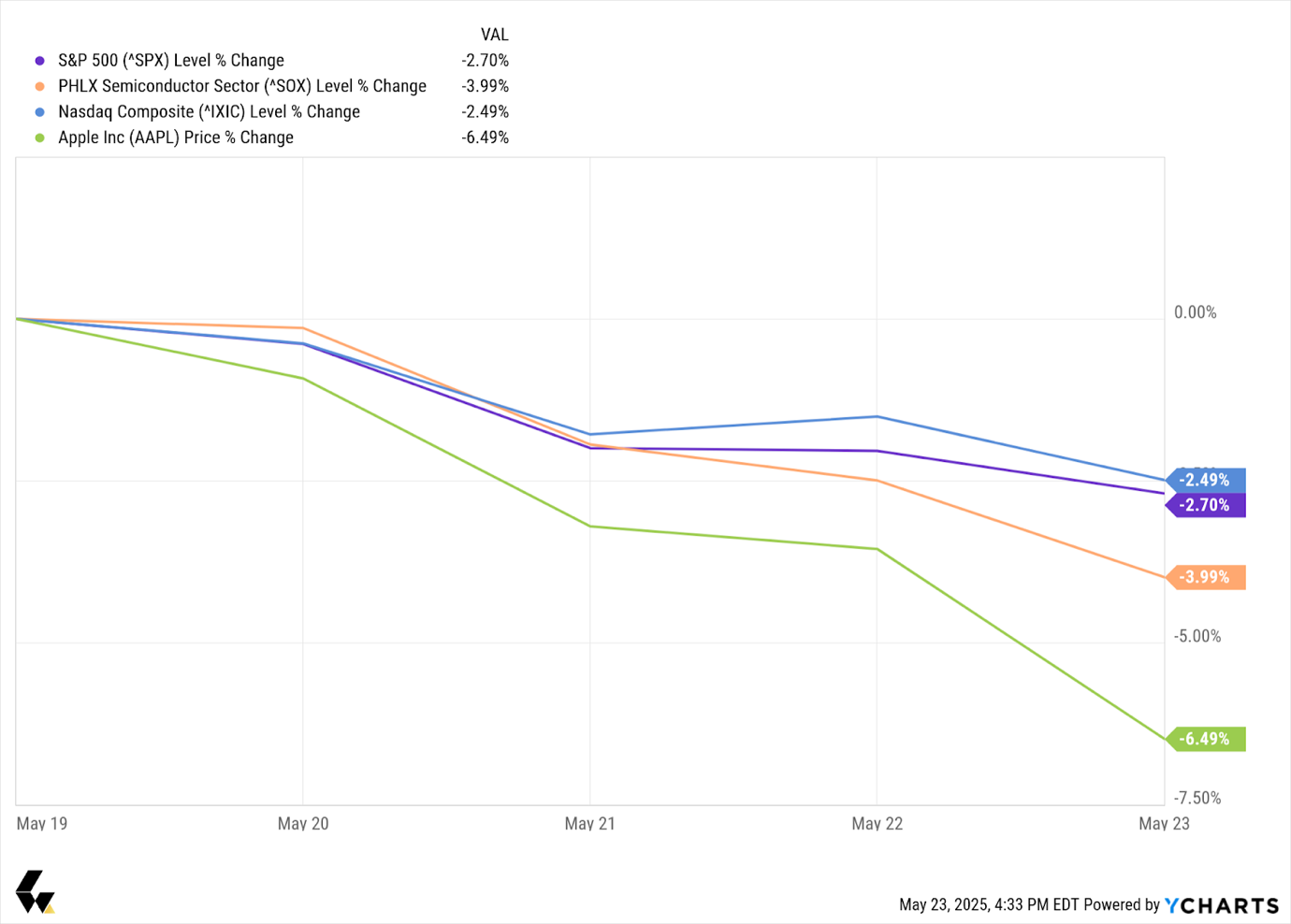

This week, major U.S. equity benchmarks extended their pullback amid political and trade uncertainties. Over the past five trading days, the Dow Jones Industrial Average fell 2.47%, the S&P 500 declined 2.61%, and the Nasdaq Composite slid 2.47%. Small caps underperformed—the Russell 2000 was down 3.47%—while the Utilities sector saw a relatively mild 0.70% drop, and the Nasdaq Biotech index bucked the trend with a 0.46% gain.

The medium-term outlook is shaped by two major developments this week: internal Republican divisions over Trump’s proposed tax-cut package and renewed tariff threats tied to his 'America First' agenda.

Quantel Asset Management’s recommendations

Building a well-diversified portfolio involves balancing short-term hedging and tactical sector opportunities with a strategic focus on long-term positioning. In the short term (30% of the portfolio), shift allocations toward gold and long-duration Treasuries to help reduce volatility, while increasing exposure to defensive sectors like utilities, consumer staples, and targeted healthcare sub-sectors. Tactical opportunities in financials, industrials, and domestic manufacturing, especially in light of potential tax cuts and ongoing reshoring trends, can be explored. At the same time, targeted investments in technology hardware firms with flexible supply chains can offer upside potential.

For the long term (70% of the portfolio), focus can be on advanced technology enablers such as AI, automation, and robotics firms, while also maintaining exposure to the energy and materials sectors, with careful attention to tariff-related risks. Adopt a cautious approach toward consumer discretionary, especially imported goods, while placing greater emphasis on domestically produced brands. Keeping abreast of legislative timelines, tariff changes, and Federal Reserve policy will be essential for effective risk management and adjusting strategies.

1. House Clears ‘One Big Beautiful Bill Act’ After Concessions, Markets React

Stocks dipped midday as rising Treasury yields and renewed doubts over the fate of a broad tax-cut package rattled investors on Wednesday.

Rare Overnight Hearing Reveals GOP Rift

In a highly unusual move, the House Rules Committee convened at 1 a.m. EDT to debate the so-called “big, beautiful bill,” highlighting deep divisions within the Republican Conference. Hard-liners in the House Freedom Caucus have stalled progress—demanding sharper rollbacks of green-energy credits and stricter spending offsets for Medicaid and SNAP—while members from high-tax coastal states push to raise the SALT deduction cap from $10,000 to $30,000. With both sides locked in disagreement, Speaker Mike Johnson acknowledged a full-house vote might slip past Wednesday.

Narrow Passage & Market Response

On May 22, 2025, the U.S. House passed the One Big Beautiful Bill Act by a 215–214–1 vote—securing support through last-minute concessions that raised the SALT deduction cap from $30,000 to $40,000 for taxpayers earning under $500,000 and accelerated Medicaid work requirements to late 2026 to win over GOP holdouts. Stocks, which had sold off amid rising Treasury yields and legislative uncertainty, steadied by Thursday afternoon as investors digested the narrow passage of bill and turned attention to the Senate’s expected revisions and the bill’s estimated $3.8 trillion impact on the federal debt.

What’s in the Bill—and Why Trump Wants It

The legislation would:

-

Extend and expand President Trump’s 2017 tax cuts for individuals and corporations.

-

Introduce new breaks on tips and overtime pay.

-

Boost SALT deductions to a $30,000 cap.

-

Tighten work requirements for Medicaid and SNAP recipients.

-

Roll back certain green-energy tax credits.

-

Increase funding for border security and defense.

The White House defended these measures stating these will spur growth, lift household disposable incomes, and enhance U.S. corporate competitiveness.

Looking Ahead: Rally Potential vs. Debt Concerns

Analysts have highlighted that the legislative package could potentially impact the federal deficit by $3.8–5 trillion over ten years. While this has influenced bond markets and led to a credit rating adjustment by Moody’s, it is also important to consider that such investments could stimulate economic growth and have long-term benefits. Historically, similar packages have had varied impacts on the economy, balancing short term fiscal challenges with potential long-term gains. A smooth passage might spark rallies—particularly in rate-sensitive financials and industrials - but investors should brace for continued volatility as amendments and vote timing remain in flux.

2. Tariffs: Short-Term Shocks & Long-Term Ripples

President Trump’s revival of sweeping import taxes has injected fresh uncertainty into global markets. We track four key episodes and highlight where to place illustrative figures.

- 2018 Steel & Aluminum Tariffs

- Policy Snapshot: In March 2018, Trump imposed a 25% tariff on steel and 10% on aluminum under national security grounds.

- Short-Term Shock: U.S. steel prices jumped ~5% and aluminum ~10% within a month, outpacing global peers and pressuring construction and manufacturing stocks.

- Long-Term Ripples: By 2019, U.S. steel output rose 6 million MT and aluminum 350,000 MT, while mill employment climbed 6–5%. However, elevated input costs slowed downstream GDP growth through 2019.

- April 2025 “Liberation Day” Tariffs (“1.0”)

- Policy Snapshot: On April 2, Trump declared a national emergency and slapped a 10% tariff on nearly all imports effective April 5, with reciprocal rates of 11–50% on 57 partners (largely suspended hours later).

- Short-Term Shock: Equities plunged on April 3, forcing rapid tariff suspensions to calm panic.

- Long-Term Ripples: The Penn Wharton Budget Model projects a 6% hit to long-run GDP and a $22,000 lifetime wage loss per median household; higher yields crowd out private capex.

- April 2025 “2.0” Baseline Tariffs

- Policy Snapshot: A tiered scheme imposed a 10% baseline on all imports (April 5) plus country-specific levies up to 50%, later adjusted through May with selective suspensions.

- Short-Term Shock: The staggered rollout and frequent reversals drove the Economic Policy Uncertainty Index to multi-year highs.

- Long-Term Ripples: Corporates accelerated near-shoring and “friend-shoring,” while policy volatility complicated long-term planning.

- May 2025 EU & iPhone Tariffs

- Policy Snapshot: On May 23, Trump threatened 50% duties on EU goods (effective June 1) and 25% tariffs on iPhones unless Apple shifts production stateside.

- Short-Term Shock: Apple shares plunged ~3%, dragging semiconductor suppliers lower as funds rotated into Treasuries and gold.

- Long-Term Ripples: Prolonged levies could fracture tech supply chains—accelerating assembly relocation to India, Vietnam, and Mexico—and provoke EU retaliatory duties on U.S. agri-exports.

3. Synthesis & Strategic Takeaways

30% of Portfolio: Short-Term Hedging & Tactical Sector Plays:

- Fixed Income & Gold: Rotate into long-duration Treasuries and gold to buffer volatility.

- Defensive Sectors: Overweight utilities, consumer staples, and select healthcare sub-industries.

- Financials & Industrials: Primed for relief rallies if tax cuts pass—consider targeted overweight.

- Domestic Manufacturing: Benefit from reshoring trends—explore ETFs or individual names with strong U.S. footprints.

- Technology Hardware: Selective exposure to companies capable of agile supply-chain shifts.

70% of Portfolio: Long-Term Positioning:

- Technology Enablers: Companies focused on AI, Automation, robotics

- Alternatives: industrial real estate assets in Mexico/Poland as potential winners.

- Energy & Materials: Monitor steel and aluminum producers in light of repeat tariff risks; favor low-cost producers.

- Consumer Discretionary: Cautious approach on goods reliant on imports; tilt toward home-grown brands and services.

Monitor Events & Manage Risks:

- Legislative Calendar: Track House/Senate vote schedules and potential amendments to tax proposals.

- Tariff Announcements: Watch White House communications for new levies or suspensions.

- Fed Policy: Let tariff-driven inflation data inform rate path expectations; adjust duration and yield curve exposure accordingly.

4. Addendum

Sources

- Reuters; USA TODAY; Reuters; Wikipedia; Penn Wharton Budget Model; Trade Compliance Resource Hub; NPR; WSJ; Bloomberg

EXPLORE MORE POSTS

AI Infrastructure Faces a Technical Reset as Markets Reassess Capex Expectations

Following last week’s discussion around more selective AI leadership, this week...

Read More

The Hidden Tax Drags Quietly Eroding Your Wealth

For investors, the conversation about returns tends to center on asset...

Read More

AI Demand Remains Strong Despite Sector Rotation in U.S. Markets

Last week, we discussed how the market continued to climb despite macro...

Read More

When Advisors Should Not Act

In financial services, we glorify action. We celebrate the advisor who spotted...

Read More

Falling Oil Prices Ease Inflation as Federal Reserve Signals Higher Interest Rates

This week, Markets experienced significant volatility as investors balanced...

Read More

Mid-Year Portfolio Review: A Practical Wealth Checklist for Investors

Most investors schedule annual portfolio reviews. However, waiting until...

Read More

Markets Turn Volatile as Growth Concerns and Geopolitical Risks Return

Markets remain caught between strong economic growth, AI-driven investment...

Read More

Why Doing Nothing Is Sometimes the Best Investment Move

SpaceX IPO Takes Center Stage as Markets Remain Near Record Highs

Markets held near all-time highs this week, but the real story was the...

Read More

Mid-Year Portfolio Rebalancing for RIAs: Turning Market Drift Into Strategic Discipline

RIAs seeking greater visibility into portfolio risk, allocation changes, and...

Read More

Markets at Record Highs: AI Stocks Lead on Strong Earnings

U.S. equities reached new record highs this week, driven by easing...

Read More

Why RIAs Must Articulate a Philosophy —Not Just Products

In wealth management, products can be replicated. Investment philosophies...

Read More

Markets Continue Higher Despite Macro Headwinds: Why Investors Remain Focused on Growth

The stock market continued its upward march this week despite facing several...

Read More

Are You Managing Wealth or Managing Chaos?

There is a version of wealth management that looks like control — scheduled...

Read More

AI Infrastructure Momentum Continues Despite Rising Treasury Yields and Global Macro Risks

After last week’s AI infrastructure-driven equity rally, investor attention...

Read More

Why Smarter Financial Intelligence Matters More Than Ever

AI should not just function as a marketing layer it should operate as an...

Read More

AI Infrastructure Leads as the Market Heats Up Again

The rally in U.S. equities continued this week, but the real strength came from...

Read More

Building Client Trust in Volatile Markets

Market volatility is not merely a financial phenomenon it is a psychological...

Read More