Japan’s shift toward tightening has added volatility to global markets, but structural support from U.S. growth, disinflation, and pending Fed easing is keeping risks contained. Unless Japanese yields or the yen move sharply, U.S. equities should navigate the turbulence and maintain a constructive setup into early 2026.

Japan’s Policy Shift Sends Global Markets Reeling

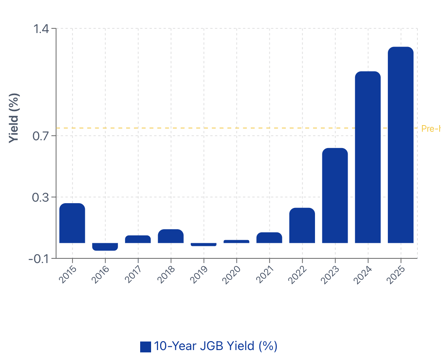

The U.S. stock market is under pressure this week as the Bank of Japan’s move on a possible December rate hike rattles markets worldwide. Japanese government bond yields have climbed to their highest levels since 2007, with the 10-year JGB approaching 1.93%, reflecting growing confidence that the BOJ will raise its policy rate to 0.75%. For a country that kept rates near zero for more than two decades, this shift represents a meaningful tightening in global financial conditions. Governor Ueda’s remarks that the BOJ will evaluate the “pros and cons” of a hike were interpreted as a signal of intent, immediately lifting global yields and tightening liquidity at the margin.

Impact of Rising Japanese Yields on U.S. Equities

Two mechanisms have driven the U.S. market’s reaction. First, higher Japanese yields reduce the relative attractiveness of U.S. assets, pushing the U.S. 10-year Treasury yield back above 4.1% and weighing on long-duration equities. Second, the prospect of a stronger yen has revived concerns about a partial unwind of yen-funded carry trades, a primary funding channel for global risk assets over the past decade. While the moves are far smaller than the August 2024 episode, the sensitivity of crypto, FX, and high-beta equities to these shifts shows how central Japanese liquidity remains to the broader market ecosystem.

Why a Disorderly Shock Remains Unlikely

For now, the risk of a sudden shock is small. Japanese investors are still purchasing foreign bonds, and lower hedging costs should keep their overseas flows steady. Japan’s policymakers have also emphasized that real rates remain negative, suggesting that even with a hike, financial conditions will remain accommodative. These factors help explain why global markets have experienced volatility, but not panic.

Supportive U.S. Macro Conditions Amid BOJ Tightening

In the U.S., the macro backdrop remains supportive. Disinflation is progressing, wage pressures are moderating, and markets are pricing in a high likelihood of a Fed rate cut next week. Equity sentiment is more fragile after a strong November performance, but underlying fundamentals—corporate earnings resilience, improving real incomes, and a potential Fed easing cycle—continue to anchor medium-term outlooks.

Near-Term Volatility, Constructive Outlook for 2026

In the coming weeks, U.S. equities are likely to stay volatile as markets assess the BOJ’s December 18–19 meeting and the Fed’s policy signals. However, unless Japanese yields break decisively above 2% or the yen appreciates in a disorderly way, any spillover into U.S. risk assets should remain contained. Overall, the U.S. macro backdrop—stabilizing growth, easing inflation, and gradually more accommodative policy—supports a constructive start heading into 2026.

Key Takeaways

-

Risks to watch: Japanese 10-year yields surpassing 2%, disorderly yen appreciation

-

U.S. equities outlook: Likely resilient amid global volatility

-

Macro drivers: Stabilizing growth, moderating inflation, potential Fed easing

EXPLORE MORE POSTS

AI Stocks Pull Back, but the Long-Term AI Investment Story Remains Intact

The AI trade paused this week as investors took profits in semiconductor and AI...

Read More

Semiconductors Pull Back, but Investor Demand Remains Strong

Despite a sharp correction in semiconductor stocks, long-term confidence in the...

Read More

Why Long-Term RIAs Outperform Short-Term Thinkers

Markets move by the minute. Headlines change by the hour. But wealth is built...

Read More

AI Infrastructure Faces a Technical Reset as Markets Reassess Capex Expectations

Following last week’s discussion around more selective AI leadership, this week...

Read More

The Hidden Tax Drags Quietly Eroding Your Wealth

For investors, the conversation about returns tends to center on asset...

Read More

AI Demand Remains Strong Despite Sector Rotation in U.S. Markets

Last week, we discussed how the market continued to climb despite macro...

Read More

When Advisors Should Not Act

In financial services, we glorify action. We celebrate the advisor who spotted...

Read More

Falling Oil Prices Ease Inflation as Federal Reserve Signals Higher Interest Rates

This week, Markets experienced significant volatility as investors balanced...

Read More

Mid-Year Portfolio Review: A Practical Wealth Checklist for Investors

Most investors schedule annual portfolio reviews. However, waiting until...

Read More

Markets Turn Volatile as Growth Concerns and Geopolitical Risks Return

Markets remain caught between strong economic growth, AI-driven investment...

Read More

Why Doing Nothing Is Sometimes the Best Investment Move

SpaceX IPO Takes Center Stage as Markets Remain Near Record Highs

Markets held near all-time highs this week, but the real story was the...

Read More

Mid-Year Portfolio Rebalancing for RIAs: Turning Market Drift Into Strategic Discipline

RIAs seeking greater visibility into portfolio risk, allocation changes, and...

Read More

Markets at Record Highs: AI Stocks Lead on Strong Earnings

U.S. equities reached new record highs this week, driven by easing...

Read More

Why RIAs Must Articulate a Philosophy —Not Just Products

In wealth management, products can be replicated. Investment philosophies...

Read More

Markets Continue Higher Despite Macro Headwinds: Why Investors Remain Focused on Growth

The stock market continued its upward march this week despite facing several...

Read More

Are You Managing Wealth or Managing Chaos?

There is a version of wealth management that looks like control — scheduled...

Read More

AI Infrastructure Momentum Continues Despite Rising Treasury Yields and Global Macro Risks

After last week’s AI infrastructure-driven equity rally, investor attention...

Read More